YEL insurance, i.e., the entrepreneur’s pension insurance

When is YEL insurance mandatory, and how much does it cost? And what is YEL income?

YEL insurance, or the entrepreneur’s pension insurance, is a statutory insurance that must always be acquired if its conditions are met.

In this guide, we have compiled all the most essential information about YEL insurance and its purchase.

Article contents:

- What does YEL insurance mean, and how does it affect?

- When is YEL insurance mandatory?

- The YEL law was reformed – how did the entrepreneur’s pension insurance change?

- What is the price of YEL insurance?

- What does YEL income mean?

- Why do many entrepreneurs deliberately underestimate their YEL income?

- How is YEL insurance purchased, and how are YEL payments made?

- What happens if an entrepreneur doesn’t take YEL, even if they are obliged to?

- Purchase YEL insurance online

If you’re looking for a YEL-calculator, you can find a link to it at the bottom of the page.

What is YEL insurance, and how does it affect?

Entrepreneurs must take care of their own pension security. For this reason, there is the entrepreneur’s pension insurance, often referred to more briefly as YEL insurance.

In practice, every entrepreneur is legally obliged to take it for themselves under certain conditions. The insurance must be acquired within six months of starting a YEL-related business.

It is a statutory or mandatory insurance, and no existing voluntary insurance removes its requirement. YEL insurance is the foundation of all social security for entrepreneurs, and its purpose is also to secure income after working life for both you and your family.

In practice, this means that you will receive income when business decreases or ends due to illness, unemployment, or normal aging.

For your family, it guarantees the right to an adequate family pension if you pass away. Maternity and paternity allowances are also calculated based on YEL.

It’s about much more than just your pension.

This is challenging, but at the same time great, because you can influence the level of your social security.

Let’s look at the situations where, as an entrepreneur, you must acquire YEL insurance.

When is YEL insurance mandatory?

The entrepreneur’s pension insurance or YEL insurance is mandatory if you meet these conditions:

- you are 18-67 years old*

- you work in your company, and your activity has lasted continuously for at least four months

- you are not covered by any other pension law when you operate as an entrepreneur (e.g., agricultural entrepreneurs’ MyEL)

- your work income exceeds the YEL lower limit, i.e., 9 423,09 euros (2026).

You are considered a YEL-entrepreneur if you meet the above conditions and are either:

- a private trader or sole proprietor (or a spouse working for one)

- a partner in a general partnership

- a responsible partner in a limited partnership

- a light entrepreneur.

In a limited company, an entrepreneur is considered to be a shareholder in a leading position (e.g., CEO or board member) who owns more than 30 percent alone or who, together with family members, owns more than 50 percent of the shares or the number of votes.

Indirect ownership, such as ownership through an investment company, is also taken into account.

Remember that the YEL obligation also applies to part-time entrepreneurs if only the above conditions are met.

So, for example, if you are in regular paid employment, but the value of your work input in your part-time company exceeds the YEL income, you must take YEL insurance.

However, if you have more than one company, you still only take one YEL insurance because it is a personal insurance.

- The obligation to insure has also been discussed in more detail on the pension company Varma’s website.

*The age limit is rising in stages. For those born in 1957 or earlier, the obligation to insure continues until the end of the month when the entrepreneur turns 68.

The YEL law was reformed – how did the entrepreneur’s pension insurance change?

The entrepreneur’s pension law changed at the turn of the year 2023: earnings from work are now defined more precisely and are reviewed every three years. The aim of the reform is to strengthen the protection of entrepreneurs and standardize the process of determining the YEL insurance work income among different pension companies. At the core of the reform is the determination and revision of the work income, as it is common for the entrepreneur’s declared work income not to match the actual work effort. According to studies, many entrepreneurs have a work income lower than the legislation requires, leaving their social security and pension protection lower compared to other population groups.

Although the concept of work income remains the same, the data used for its determination becomes more precise. Work income still corresponds to the salary that should be paid to another person performing the entrepreneur’s job. Work income is compared to the median salaries of workers in the entrepreneur’s sector. Other data related to the value of the work contribution are also considered in determining work income. Individual consideration and variation of the work income are still possible, and are also required by law.

The work income decision made by the pension company is significant for the entrepreneur because it affects their livelihood and YEL contributions. Since making the decision requires discretion, the role of the justifications for the decision is important. The reform requires that work income decisions are justified more clearly for increased transparency.

The biggest change is the new obligation of pension companies to check work incomes every third year. This is designed to ensure that the work income is up-to-date.

Price of YEL insurance in 2026 – how much does an entrepreneur’s pension insurance cost?

For many new entrepreneurs, the essential question is how much YEL insurance costs.

Entrepreneur’s pension insurance is paid according to a certain percentage, and the price of YEL insurance depends on this percentage.

The annually changing percentage has slight differences based on the age of the insured, but the percentage is the same in every insurance company.

So, the price remains the same regardless of which pension insurance company you choose.

In 2026, depending on your age, the figure is either 24.10 or 25.60 percent of the YEL work income. The entrepreneur defines their YEL work income themselves; we will tell more about this under the next subheading.

Note that a person starting as an entrepreneur for the first time gets a 22 percent discount on their payment. You can enjoy the discount for four years.

Price of YEL insurance in 2026 – example: Let’s imagine you’re a 30-year-old new entrepreneur and set your YEL work income to the minimum, which is 9 423,09 euros. In this case, taking into account the discount for new entrepreneurs, the annual price of the YEL insurance would be around 1600 euros if you paid the insurance premiums in 12 monthly installments. If you set your YEL work income at 20,000 euros, the insurance price would then be about 3760 euros annually.

If you wish, you can save a few euros by paying off the entire insurance premium in January. At the bottom of this page, you’ll find a YEL calculator with which you can calculate your situation-specific price.

What does YEL work income mean?

The YEL payment is based on the work income you estimate yourself. But what is YEL work income?

When you take out YEL insurance, you define your annual work contribution value, i.e., the YEL work income. The value you set should correspond to the amount of money you would pay as a salary to an external employee hired for the same job who has equivalent professional skills as you. Therefore, YEL work income does not mean the company’s profit, turnover, or the entrepreneur’s taxable income, but is an estimate you make yourself.

If you sell cars, you might make a turnover of 10,000 euros with one deal in one day – of course, the value of the work effort required for that one day’s sale is anything but 10,000 euros. This is just a rough example, but hopefully, it helps you grasp the concept.

The work income you set affects how large of an entrepreneur’s pension and social security you’ll enjoy.

The minimum YEL work income for 2026 is 9 423,09 euros. If, for example, you are a part-time entrepreneur and estimate that your work income is below this limit, you don’t need YEL insurance.

If you plan to do small-scale business in the near future and know that your annual earnings will be below this limit, one good option is light entrepreneurship. You can learn more about it through the provided link.

Why do many entrepreneurs set their YEL work income too low?

Many entrepreneurs who earn above the YEL limit intentionally set their YEL work income on the low side or equivalent to the minimum limit.

A few years ago, the pension company Elo reported that at that time, every third entrepreneur had set their YEL work income so low that it didn’t provide sufficient security for retirement or unemployment.

There can be many reasons for this:

- The entrepreneur believes or knows that their retirement days are already secured in other ways.

- The entrepreneur has purchased insurance for unemployment or incapacity in other ways.

- The entrepreneur invests the saved money and believes that this way they will accumulate more money for retirement.

The situation is very specific, so we won’t speculate on which approach is profitable and which isn’t.

When paying the YEL minimum, it’s important to genuinely ensure that money is set aside for a rainy day every month.

You can apply for a change to the work income you reported if needed later on.

The underinsurance of entrepreneurs and YEL work incomes set too low have been frequently discussed in various media in recent years. Yrittäjät.fi recently reported that in the future, pension companies will more precisely guide entrepreneurs’ YEL work income to the right level. The same issue has been briefly covered in an article on YEL insurance by eTasku.fi.

How do you obtain YEL and how do you pay for it?

Acquiring the YEL insurance can be most easily done on the website of any pension insurance company.

Of course, you can also contact the customer service of the pension insurance company by phone if for some reason you do not want to fill out the insurance application yourself.

Pension insurance companies in Finland include:

- Elo

- Veritas

- Ilmarinen

- Varma.

To obtain YEL insurance online, you primarily need online bank credentials or a mobile certificate, which you use to authenticate to the service.

Once you have obtained the insurance, you will receive YEL payments as bills either electronically or on paper.

As we mentioned earlier, the YEL payment percentages are the same in every pension insurance company, so the price remains the same regardless of which company you take your insurance from.

When are YEL payments made?

You can pay the YEL insurance premium in installments of your choosing.

Options are 1, 2, 3, 4, 6, or 12 installments, so if desired, you can spread payments for each month or pay everything off at once.

You can also change the payment rhythm via online services.

YEL insurance payments are fully deductible in taxation.

You can deduct them in either your personal or your company’s taxation depending on who has paid the YEL payments.

Deductibility means that YEL payments are deducted from taxable income. They therefore reduce the amount on which tax is paid. As a result, the amount of tax payable also decreases.

What happens if an entrepreneur does not take YEL insurance even though they are obligated to?

The obligation for YEL is supervised by ETK, the Pension Security Centre.

They obtain information about your activities, for example, through your earned income and your company’s tax information.

If these details reveal that you might be obliged to take the entrepreneur’s pension insurance, the ETK will give you a reminder.

If the reminder is ineffective and further investigations reveal that you are obliged under YEL, the ETK will take out insurance on your behalf, in other words, they will compulsorily insure you.

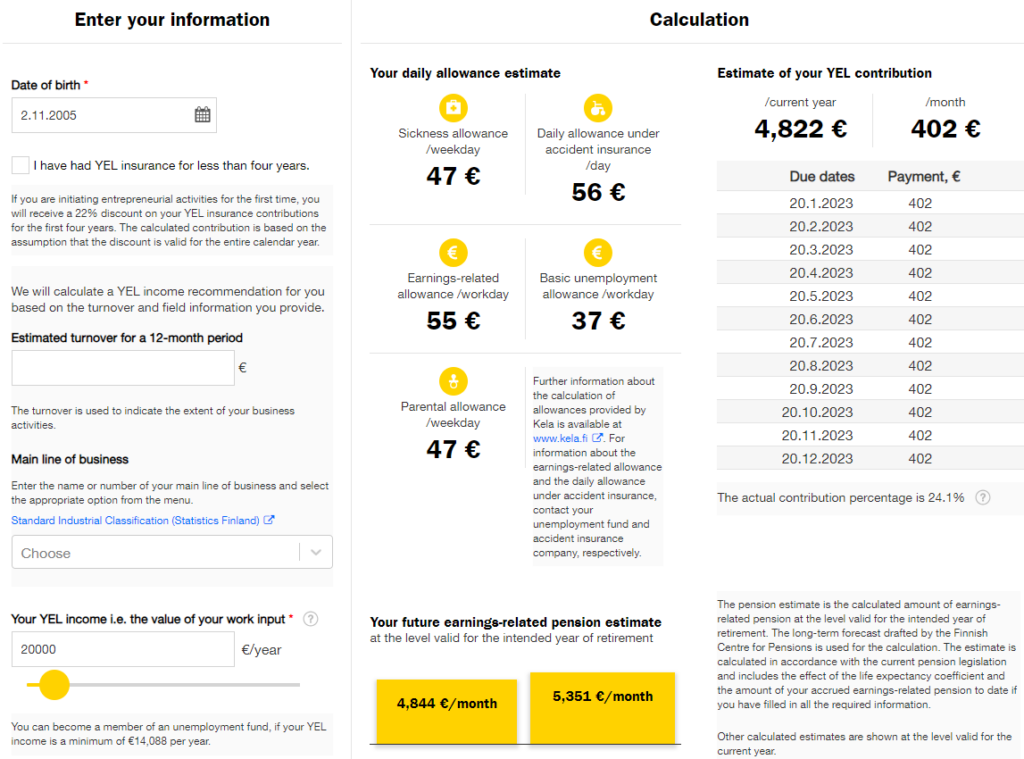

YEL calculator for YEL insurance

You can find the YEL calculator on the pension insurance company Elo’s website. Below is an indicative example image of the calculator. You can see the up-to-date amounts from the calculator.

Sample prices for YEL insurance can also be read earlier in this text.Easily get YEL insurance online

Ota YEL-vakuutus helposti verkossa

Taking entrepreneur’s pension insurance is easily done online through the websites of the pension insurance companies. If obtaining insurance is relevant, you can fill out the YEL insurance application through the following links.

Which pension insurance company do you want to get your insurance from?